CIPA has posted the final numbers for 2016, and it's one of those good news, bad news things. The good news is that the Japanese companies were very active at the end of the year for a change, probably trying to make up for lost shipments during the sensor shortage caused by the quake earlier in the year.

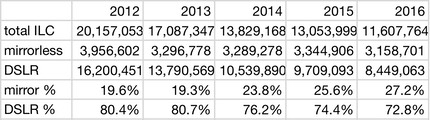

Thus, when you look at mirrorless and DSLR shipments for the last quarter of the year, they were up 13.1% and 1% respectively compared to the prior year. But here's the full year stats on interchangeable lens camera (ILC) shipments:

While mirrorless is holding relatively steady for the past four years, DSLRs have dropped significantly. We're now down to half the number of DSLR shipments as we had five years previously.

As I reported earlier this week, Canon is now claiming 50% of the ILC shipments for 2016. We won't know what Nikon claims until Valentine's Day (actually the day before), but I'm betting it won't be a love fest. It could easily be 25% or lower.

I had estimated 3.5m mirrorless units for 2016 before the quake. I still think that mirrorless is on a mild growth path and should hit at least that in 2017.

The question is where are DSLRs going? And in particular, where are Nikon DSLRs going? (That's because Canon reported flat DSLR sales for 2016, so the 13% drop CIPA reported was all Nikon, Pentax, and Sony.)

If not having a viable mirrorless entry was trouble for Nikon in 2016, it's now a crisis in 2017. Either that or they need to reprove that DSLRs have growth, which given the recent D3400 and D5600 updates, well, just ain't happening.

Nikon, in particular, is firing on almost no cylinders at the moment. DL? Didn't show up. DSLRs? Good start with the D5/D500, nothing interesting after that. Mirrorless? All quiet on the Eastern front. KeyMission? Late to the game, and a clear foul ball when they got to bat. Coolpix? Not so cool. Other than the D5/D500, about the only good thing you can say about Nikon's 2016 was that the few new lenses they launched were all excellent, though pricey.

The way I'd codify the current status of the companies:

- Canon — found a groove and going with it. 1" for compacts, solid APS mirrorless getting more attention, keep the DSLRs iterating on schedule. Video as their special added market.

- Fujifilm — continuing to rise from the bottom after they stepped away from the market. Great APS and MF combo brackets the full frame DSLRs nicely. Lots of attention to lenses and improvement.

- Nikon — said it above: they're in crisis. They need a strategy, they need new models, they need a new mirrorless system, they need...there's not much they don't need.

- Olympus — finally pared to the bone, and building marrow on it. Not a lot of muscle. Moreover, it's a single bet on the Come line.

- Panasonic — seems all-in on the still-camera-is-a-video-camera thing, and owning it well. Video is also their special added market (e.g. Varicam).

- Pentax — the one thing they got to first (50mp MF) isn't as cool as the ones that got there last; everything else is much the same as Nikon.

- Sony — strange year for them, as obviously they're 100% reliant on sensors from the fab that went down. The pace of their fanatic iteration slowed, and I think it'll stay a bit slower now (but watch for the triple stack Exmor that's coming). They've solidified their place as third in ILCs, and if Nikon keeps collapsing, that'll be second will no further changes on Sony's part. Video is also their special added market, particularly since their still and video lines fully share a lens mount now.

So. Completely healthy? Canon and Sony. Getting healthy? Fujifilm and Panasonic. Recovering? Olympus. AWOL? Nikon and Pentax.